The age of the solopreneur

More solo founders, growing faster, powered by AI

The US Census Bureau counts businesses as well as people. Four years ago, it made a major change to its business methodology. Until 2022, the Census Bureau assumed that businesses over a given revenue threshold must have employees. Even if a business declared itself a solo enterprise, it was automatically reclassified as an employer when it hit a certain income threshold.

By the early 2020s, these assumptions started creaking. The Census Bureau noticed that solo operators in some sectors were generating substantial revenue, and they didn’t seem to be hiring. And so in 2022, the Census Bureau systematically raised its income thresholds. The resulting counts of nonemployer businesses at higher income levels skyrocketed.

Today, Census Bureau Business Formation Statistics, cross-country business registration records, and Stripe platform data all suggest solopreneurs have continued to prosper.

This post advances three related arguments. First, solopreneurship is growing faster than employer-business formation, and the acceleration is validated by multiple independent data sources, making it unlikely to be driven by a fraud wave. Second, both the number and share of solopreneurs reaching meaningful income thresholds is rising. And third, early signals indicate that AI is filling the capability gaps that once made hiring necessary—and doing so fast enough to show up in the income distribution.

Solopreneurs are multiplying much faster than employer businesses, and it’s not fraud

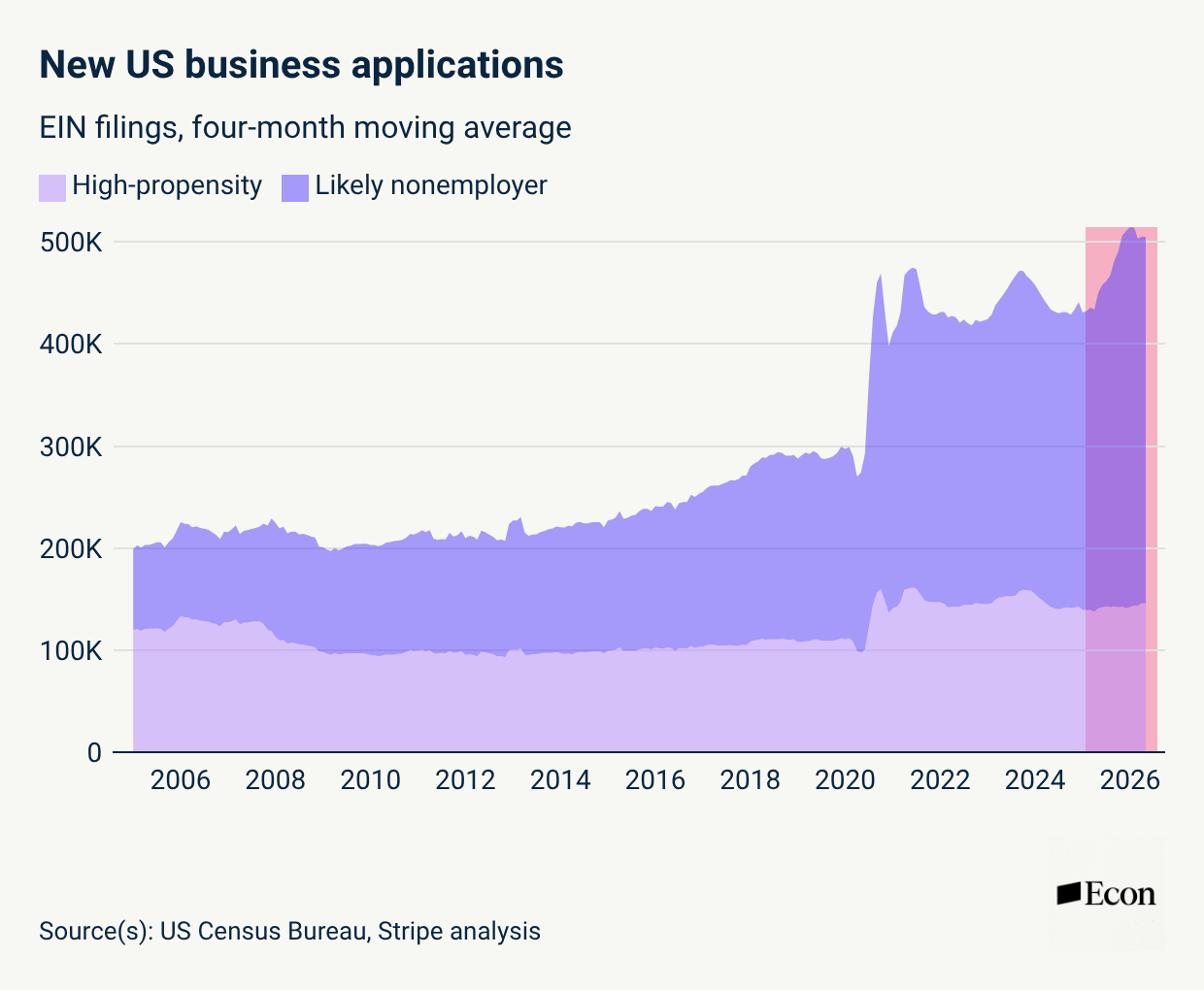

New business applications in the Census Bureau’s Business Formation Statistics have been flashing an unusual signal for the past 18 months. New business applications are filings with state agencies and the Internal Revenue Service that precede actual commercial activity. These new applications reaccelerated beginning in late 2024, after spiking in 2020 at the beginning of the pandemic and remaining elevated thereafter.

This acceleration, however, is not being driven by applications from businesses that have a “high propensity” or likelihood to become employers. The Census Bureau classifies certain new business applications as “high propensity” if it deems the business as likely to hire workers within the next eight quarters. The Census Bureau uses an internal statistical model that considers industry classification, whether an Employer Identification Number (EIN) was requested, and whether the applicant indicated planned wages. High-propensity filings have stayed relatively stable over the past 18 months even as overall applications have surged.

A similar spike in new business applications occurred early in the pandemic. The Paycheck Protection Program (PPP) was a small business loan program that the US federal government established in 2020. It required an EIN and little else for eligibility, creating strong incentives for applications with no genuine entrepreneurial intent. Economic research has found a contemporaneous increase in the composition of 2020 applications toward businesses likely to be nonemployers (Dinlersoz et al. 2021). The nonemployer surge peaked and partially reversed as the PPP program wound down—though interestingly, the level of business formations in the US stayed persistently higher than prepandemic.

For the current acceleration in new business applications, there is no comparable federal subsidy creating a financial incentive to file. The PPP stopped accepting new applications in May 2021, and the last forgiveness payout was in 2024.

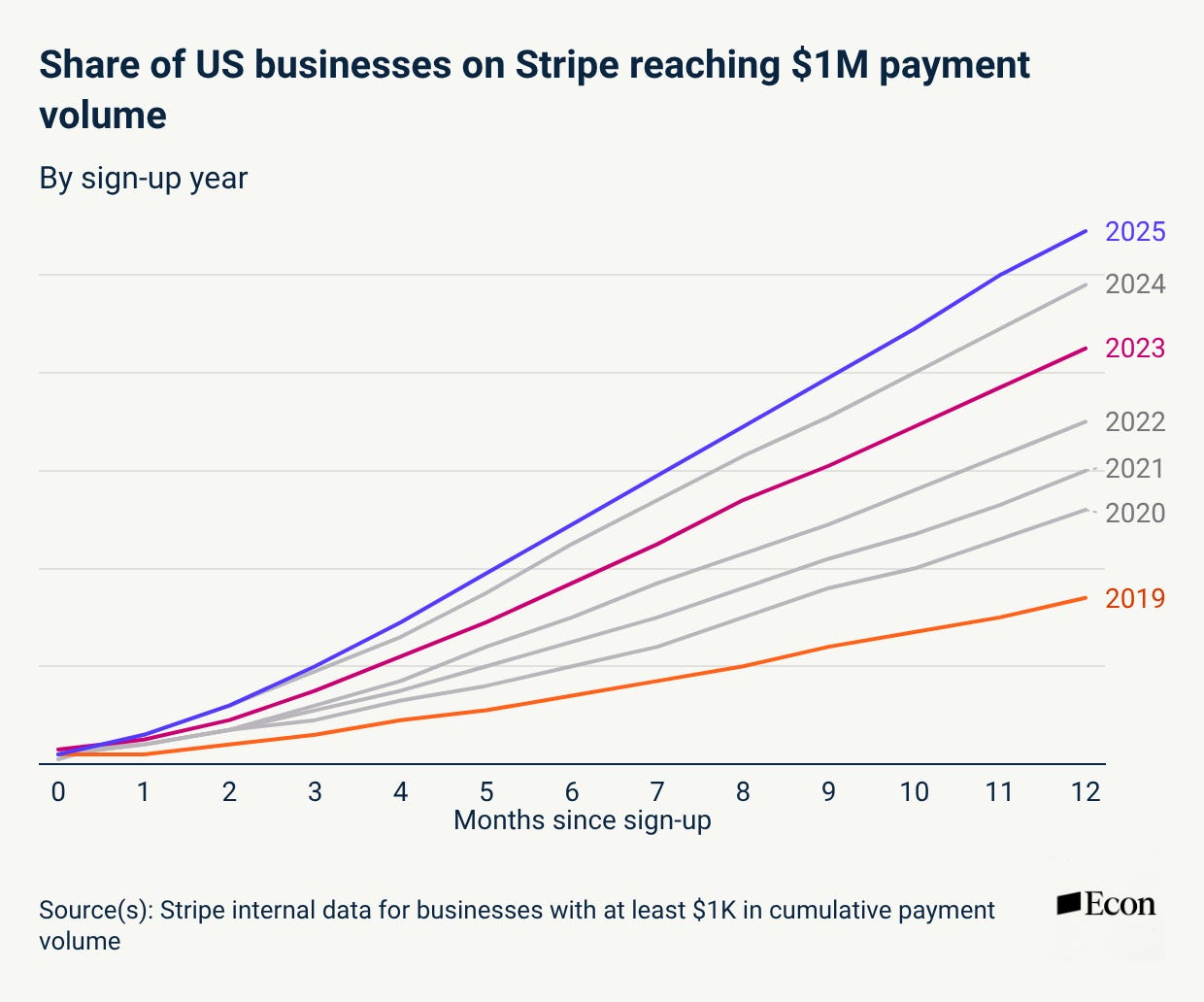

Three further pieces of evidence argue against fraud specifically. The first is that Stripe pay-in data is also consistent with the read that recent business sign-ups are legitimate. Stripe cannot distinguish between solopreneurs and employers among business sign-ups, but we do validate the overall acceleration and the meaningful activity of these businesses. Businesses that signed up on Stripe after 2023 reached material transaction volumes earlier than the sign-up cohorts that preceded them. The share of businesses (not just solopreneurs) reaching $1 million in cumulative revenue within a year after going live on Stripe was roughly 30% higher for the 2025 cohort as it was for the 2023 cohort, and it was roughly 3x higher for the 2025 cohort than the 2019 cohort. If more recent sign-up cohorts were increasingly driven by inactive businesses, we would expect more time to material volume thresholds, not less.

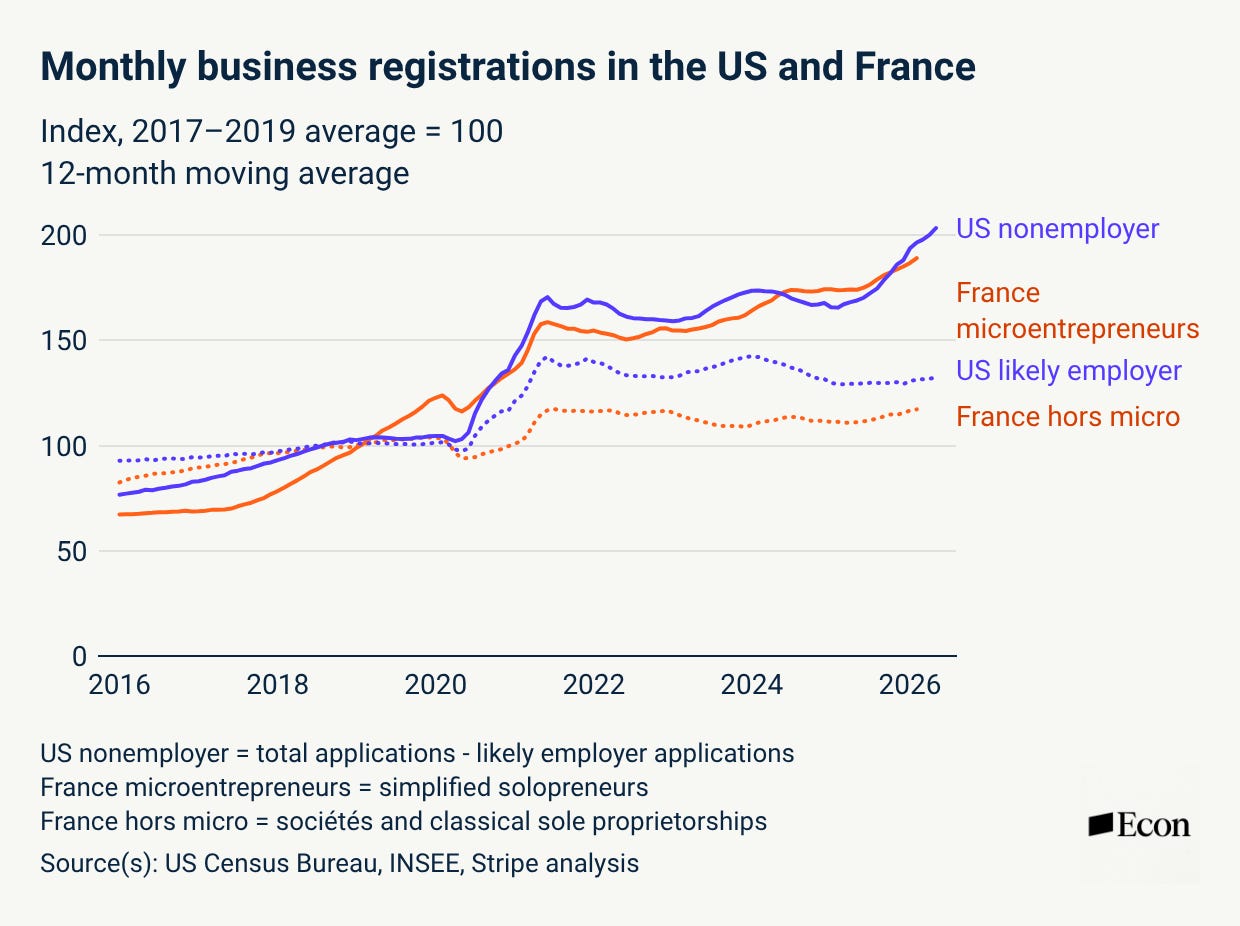

Second, as we have shown previously, the story of spiking business applications is not confined to the United States. New business registrations have risen roughly 40% in Australia, 70% in Finland, and 80% in France since 2017, with meaningful acceleration in 2025 alone. Multicountry acceleration across different regulatory environments argues for a more fundamental driver than fraud activity. And in France, where more granular data is available, the surge in business formation is driven primarily by solo founders or microentrepreneurs rather than by traditional employer businesses—similar to the US.

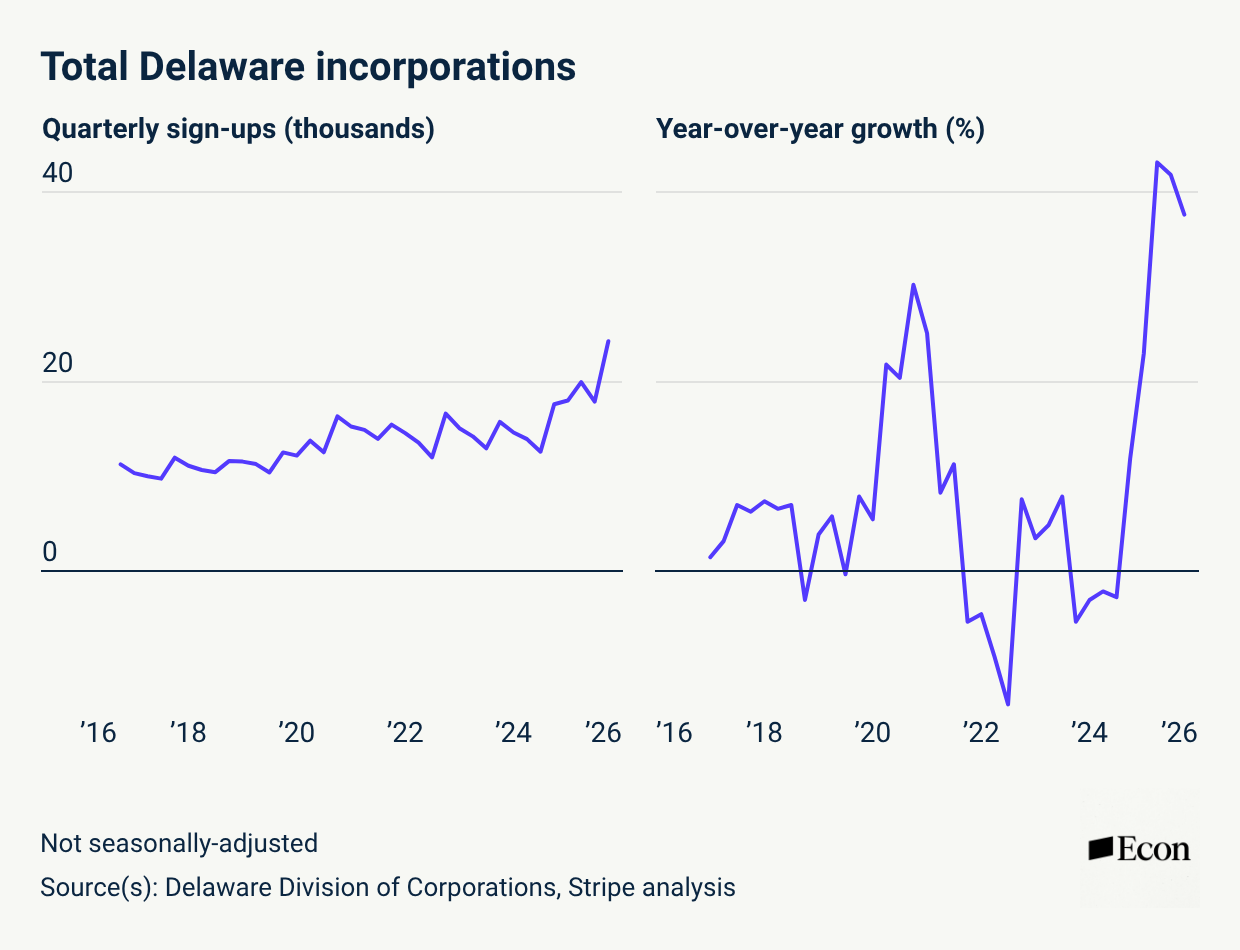

A final reason to be skeptical of fraud in the current acceleration is that we have also seen growth in incorporations in the US state of Delaware. Delaware incorporations have grown approximately 40% year over year since early 2025, and they have remained at or above the pandemic-era peak every month since January 2025. While Delaware represents only about 75,000 of the roughly 5.7 million business applications filed in the United States in 2025, it is the incorporation jurisdiction of choice for founders who intend to raise institutional capital or establish formal governance structures, making it a strong signal of genuine business intent. It is not the natural destination for a passive LLC filing by bad actors.

Business applications are also growing fastest in Wyoming, another jurisdiction associated with deliberate legal structuring rather than passive registration. The geographic composition of the acceleration tilts toward intent.

Solopreneurs at higher income thresholds are seeing rapid growth

In 2023, roughly four million Americans earned their primary income as solopreneurs, generating over $100,000 in annual revenue. That figure has risen substantially from the mid two-million range of the early 2010s, a period when the infrastructure enabling solo business at scale—Stripe, Substack, Kajabi, and other platforms—was still small in scale and more limited in capabilities. On its own, this doubling is already impressive. But what about solopreneurs at even higher income thresholds? Here, the Census Bureau’s data is unfortunately more limited. Methodological changes over the years make longitudinal studies of Nonemployer Statistics (NES) data challenging.

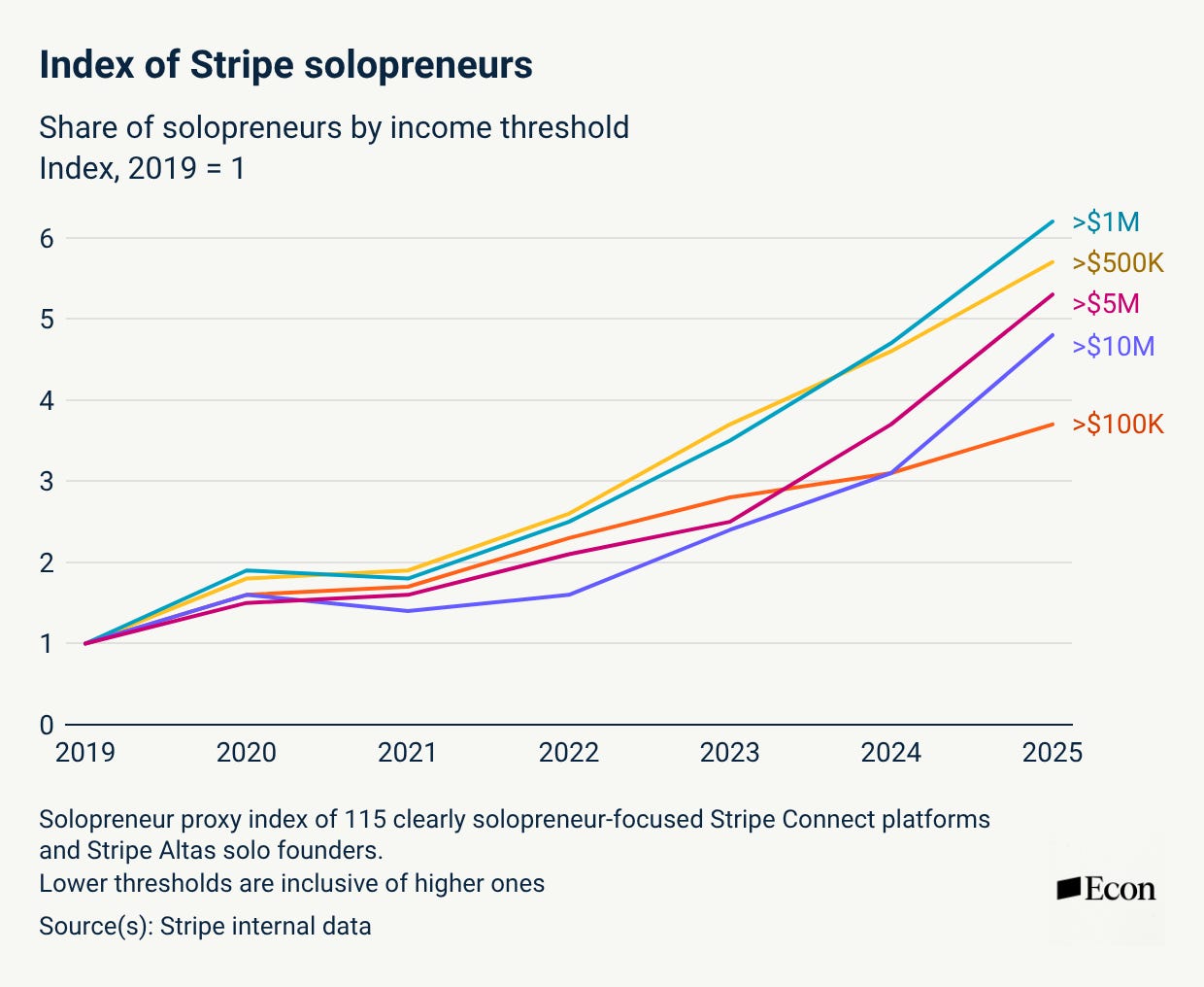

To understand what is happening with higher-income solopreneurs, we constructed a proxy index of solopreneurs on Stripe, covering approximately 115 solopreneur-focused platforms and all solo Stripe Atlas businesses. This index almost certainly understates the actual Stripe solopreneur population, since most solo operators use general-purpose infrastructure rather than solopreneur-specific platforms. But it tracks directional trends with reasonable fidelity, and it shows a consistent upward trajectory in both the count and share of solopreneurs earning above various income thresholds.

We find that there has been a substantial increase in the number of solopreneurs earning over $100,000 in our index, but an even larger increase in the number earning at higher income thresholds, with a clear acceleration since 2023. More than twice as many solopreneurs earned over $1 million in 2025 than in 2023, and close to three times as many crossed $5 million and $10 million.

Perhaps even more interestingly, the share of solopreneurs earning above these income thresholds has also doubled in the last two years, suggesting that—rather than the surge in business applications reflecting low-quality experimentation with a few lucky standouts— the cohorts of new solopreneur businesses might actually be of higher quality than in the past.

This is a proxy. There might be nonsolo businesses using these solopreneur-focused platforms. Businesses that started as solopreneurs might have since added employees. And even for those that are in fact solo, the earnings distribution within the solopreneur category is almost certainly wide. Still, these trends are quite striking and suggest a true shift in the scale solopreneurs can reach on their own and the frequency with which they do so.

AI is filling the capability gaps that once made hiring necessary

It seems likely that AI is one of the primary drivers of both the acceleration in solo business formation and the outsized performance of solopreneurs in recent years. However, untangling this effect is not always easy.

Part of the story is ease of discovery of, access to, and integration of new tools. An agent can now help you find the best tools for your business and handle your integration with minimal support. We see this effect in both Census Bureau data and our sign-up data via what we call AI-assisted sign-ups.

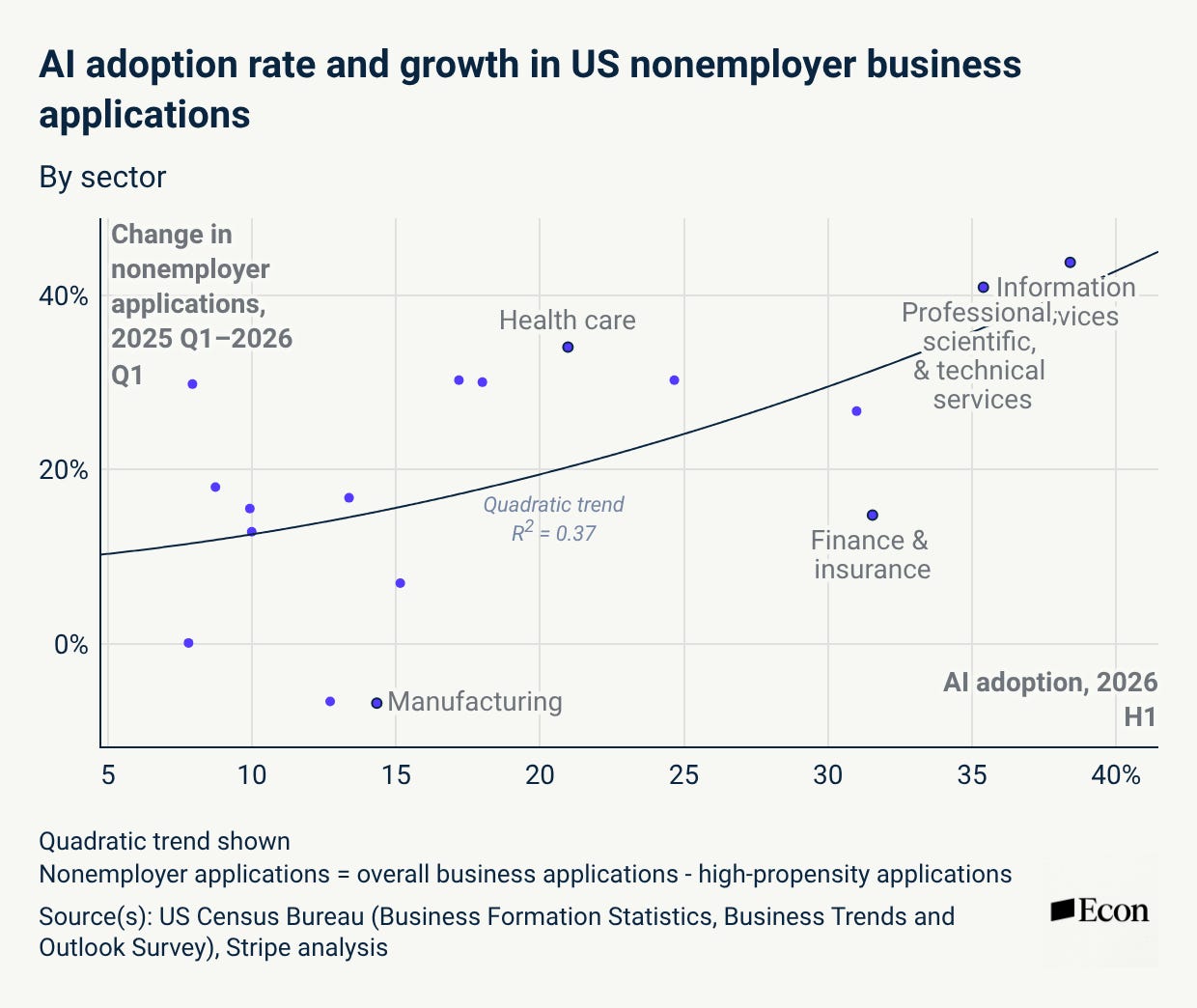

Census Bureau data allows us to dig further into nonemployer business applications, segmenting the data by broad sector. The following chart compares the percent growth in this nonemployer proxy since the first quarter of 2025—when it started accelerating—to AI adoption in the Census Bureau’s Business Trends and Outlook Survey (BTOS), which asks whether the business used AI in any of its business functions over the prior two weeks. The recent growth in nonemployer businesses shows a positive relationship with industry-level AI adoption, suggesting that higher AI adoption has been broadly consistent with more growth in nonemployer applications, though with notable outliers (manufacturing on the downside, transportation and warehousing on the upside).

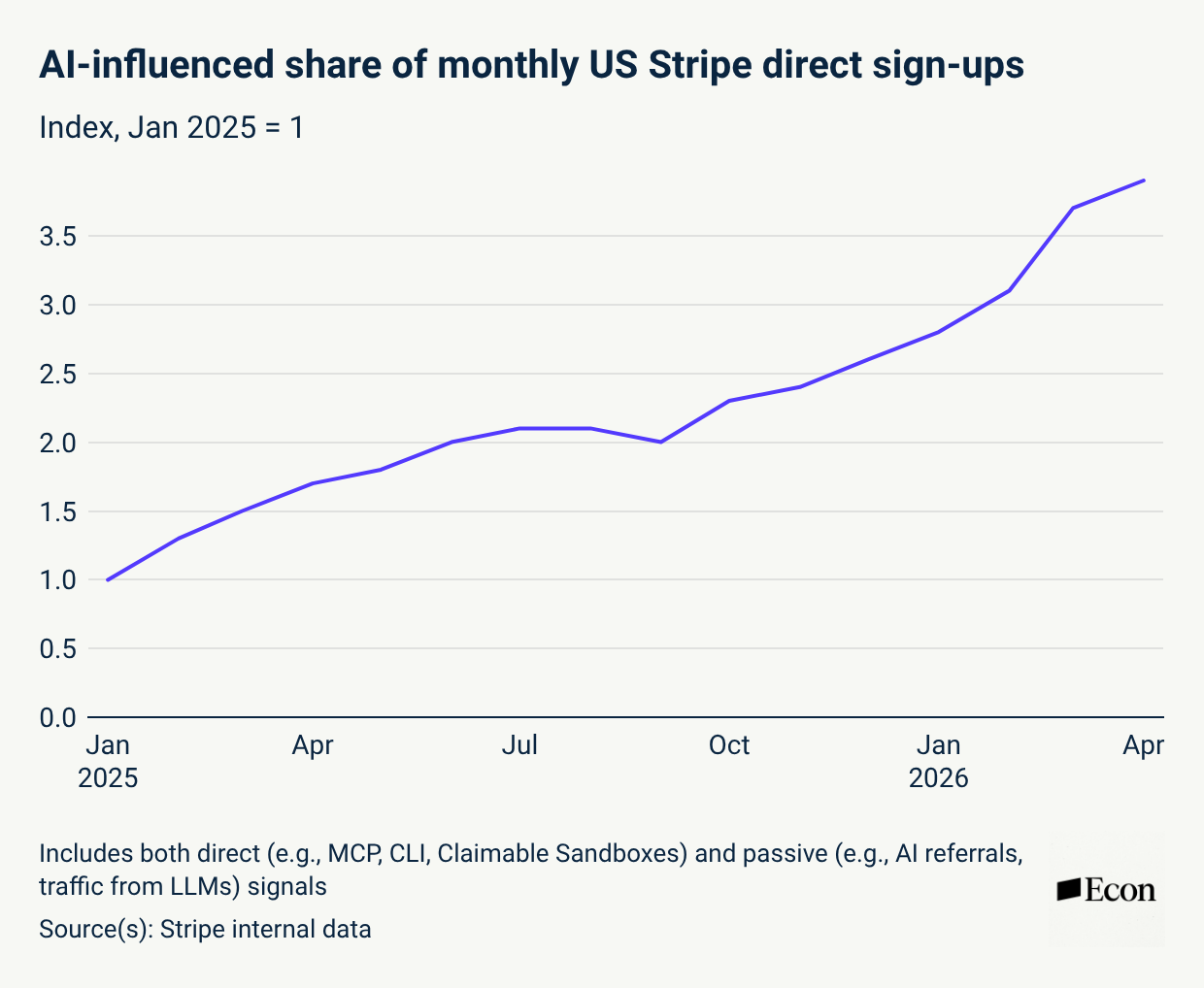

AI-influenced user journeys now constitute nearly 4x the share of Stripe sign-ups as last January. We measure two types of AI assistance among the businesses using Stripe today: direct and passive. Direct behavioral signals indicate use of AI tools to build or manage Stripe integrations. These are things like using our Model Context Protocol (MCP), command-line interface (CLI), or Claimable Sandboxes—a Stripe feature launched in October 2025 that lets prospective businesses interact with a prebuilt demo environment before formally signing up. Passive signals indicate association with AI tools but not necessarily AI-assisted building. These are things like AI referrals, or traffic arriving from large language models like ChatGPT that recommend Stripe to businesses researching how to accept payments.

These are substantial numbers; however, they likely understate the importance of AI in the solopreneur surge. Part of the reason businesses historically tended to be built by groups was that a single individual rarely possesses all the skills needed in the entrepreneurial journey. Whether it’s how to evaluate or size a market, code an app, price a product, write and execute a marketing campaign, or close a deal, AI (and AI-augmented software) can fill many of the gaps that founders previously turned to another human for. Or, as Sam Altman so succinctly put it: “revenge of the idea guys.”

We think this phenomenon is the true engine of the AI surge in business formation we’re seeing today. The availability of this breadth of on-tap assistance allows anyone with sufficient motivation to go it alone. Given this, we think the 20% figure is a floor rather than a ceiling in terms of AI impact.

Conclusion

While the recent surge in US business formation is not reflected in high-propensity applications, the evidence points toward a structural increase in genuine small business activity over 2025 and 2026, driven by solopreneurs. Preliminary evidence of growth in AI tool usage and solopreneur growth in high-AI-adoption sectors suggests that advances in AI are responsible for a meaningful portion of this growth. We believe AI is lowering barriers to business formation and growth by expanding the capabilities of solopreneurs, further improving tools and platforms that cater to new businesses, and creating a new set of opportunities for entrepreneurs to pursue. Whether the magnitude of this effect is as large as the most optimistic readings of the data suggest remains to be seen, but we believe we might be in the early innings of a fundamental acceleration in business formation—which could have ripple effects throughout the economy.

| A guest post by

|

| A guest post by

|

Awesome post - thanks for putting it together. As a one-man business, I agree with this data :) I am not hiring, and don't plan to, only because of have AI at my disposal (for editing, designing, and more). AND, Stripe makes it incredibly easy to process payments. So thank you for helping my little 1-person company run.

Really good data here — the cross-validation across Census, Stripe, and international filings makes the "this isn't fraud" case well.

One thing the AI section understates, I think: you're measuring AI's effect on the capability side (one person doing work that used to need a team). But there's a second-order effect on the discovery side that doesn't show up in this data. A team produces legibility as a byproduct — separate employee profiles, a comms function, a site someone was paid to structure.

A solopreneur running real revenue off a Stripe link and not much else often has none of that residue, not because anything's wrong, but because there was never a team to leave the trail.

That was a minor disadvantage when humans did most of the finding — people fill gaps with context. It gets sharper as more discovery work (vendor search, supplier evaluation, candidate sourcing) shifts to agents reading structured data instead. Solo revenue going up and solo legibility going up are not the same curve.

Would be curious whether you're seeing anything on the discovery/search side that tracks this independently of the revenue numbers in this report.