Is the UK missing out on the solopreneur boom?

Government statistics would say yes, Stripe data suggests otherwise

In our last post, we covered the surge in solopreneurship in the US, and one reader had a good provocation.

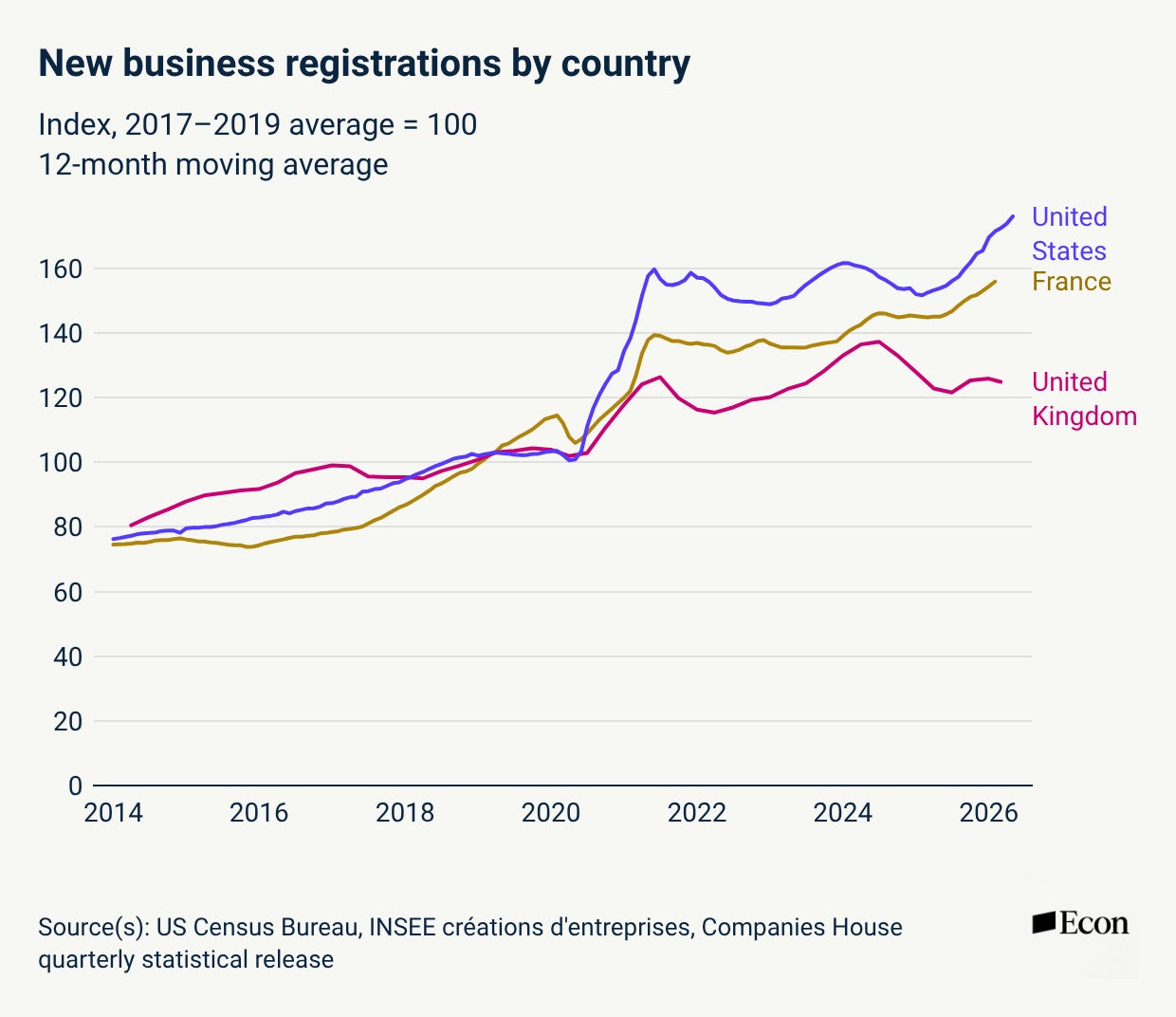

UK statistics show business creation flat or even declining over the past 2 years. Is the UK really falling behind or is something else afoot? In this appendix to our last post, we triangulate across Stripe data and public statistics, and conclude that the UK is likely seeing its own business formation boom that government statistics are simply failing to capture.

The UK lacks a clear solopreneur registration pathway

The US and France have explicit statistics related to solo or microbusinesses. The Census Bureau’s business application statistics are based on EIN filings, which, while not technically necessary to start a sole proprietorship in the US, are highly common in practice. INSEE’s data on création d’entreprises leverages the microentrepreneur regime (focused specifically on solopreneurs). The UK, however, has no such solo pathway. Companies House statistics don’t include sole proprietors or the self-employed. The Office for National Statistics (ONS) similarly only counts businesses registered for VAT or PAYE (tax withholding)—a threshold that many solopreneurs fail to meet.

The Department for Business and Trade (DBT) publishes its own business population estimate, which tries to “back out” the number of unregistered businesses (primarily self-employed and sole-traders) using the Labour Force Survey (LFS). The LFS counts people who identify as self-employed, but this likely struggles to account for individuals whose solo enterprises are a nascent or supplemental source of income—for example, a person who has a Substack or a Shopify store on the side that they monetize while still maintaining a salary job. The LFS has also been plagued by multiple issues, losing roughly half its effective sample since COVID-19 (from approximately 70,000 individuals surveyed in 2019 to fewer than 35,000 in 2023), and with worse attrition among young people who are more likely to be self-employed. The LFS publication was suspended entirely in 2023 and was relaunched in 2024, downgraded to “statistics in development” due to these challenges; the DBT statistics were then also downgraded.

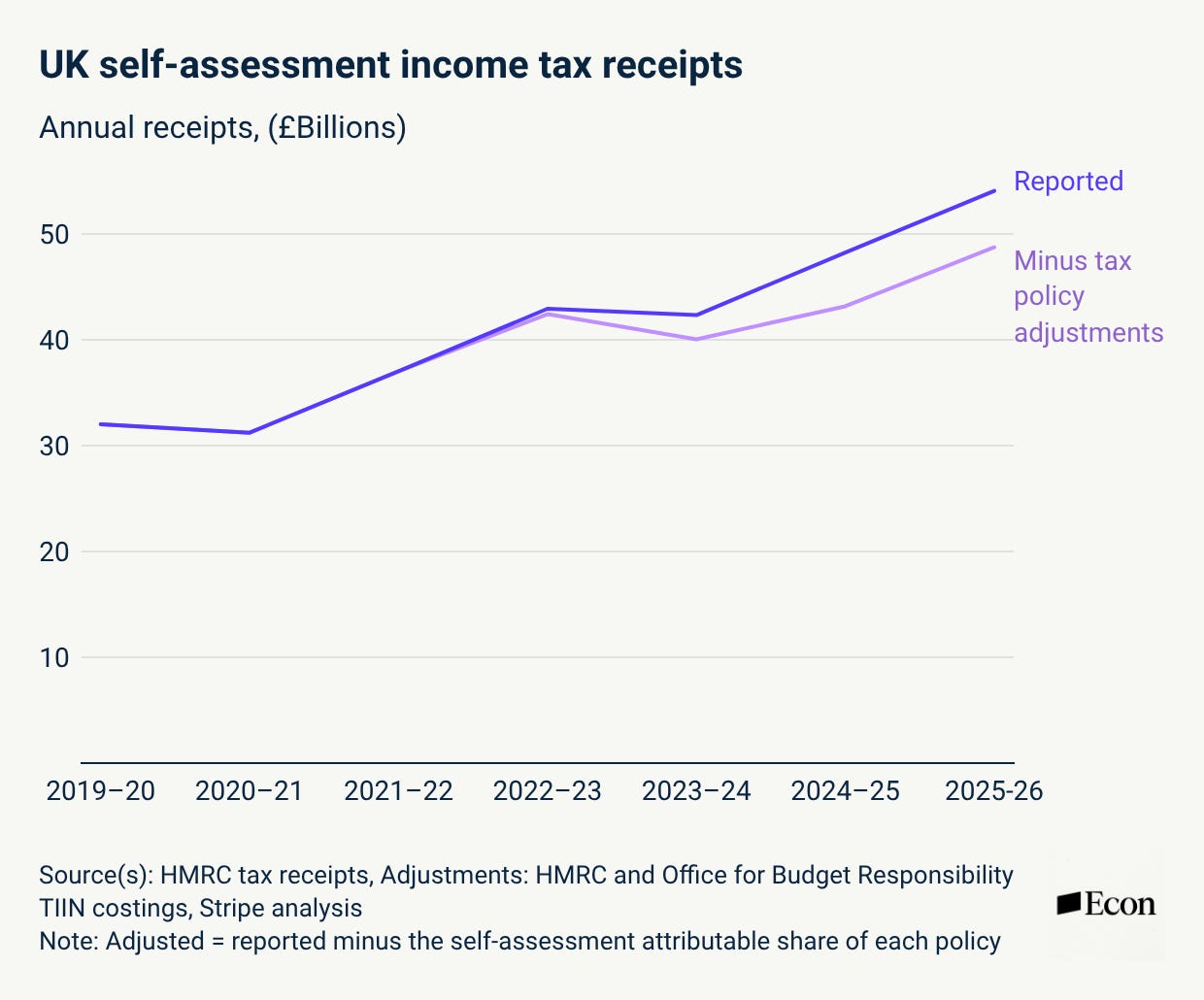

Tax receipts are broadly consistent with an increase in solopreneur activity

An imperfect proxy for solopreneurship in the UK is self-assessment income tax receipts (i.e., taxes that are paid by individuals rather than directly by employers). Self-assessment receipts increased by over 70% relative to the pre-COVID period and showed a reacceleration of 12% in the last available year of data. This is consistent with growth in solopreneur activity, if not dispositive.

There are several caveats: solopreneurs do not need to register with HMRC if they make less than £1,000, which means the data excludes a large swath of the solo population who are either early in their journey or experimenting. Individuals also file self-assessment taxes for many reasons besides self-employment (e.g., declaring property income or investment income), with changes in dividend allowances in 2023–2024 artificially increasing receipts from this category.

Finally, UK tax law until recently required earners above £100,000 to file self-assessment even if their employer paid their taxes. However, this last point—while meaningful for self-assessment filings—should not materially impact receipts numbers since the vast majority of tax for this group is captured at the source (via PAYE) rather than via the self-assessment tax return. Thankfully, HMRC tax information and impact notes (TIINs) provide data on costings for each of these recent policy changes, so we can disentangle these confounding variables relatively cleanly.

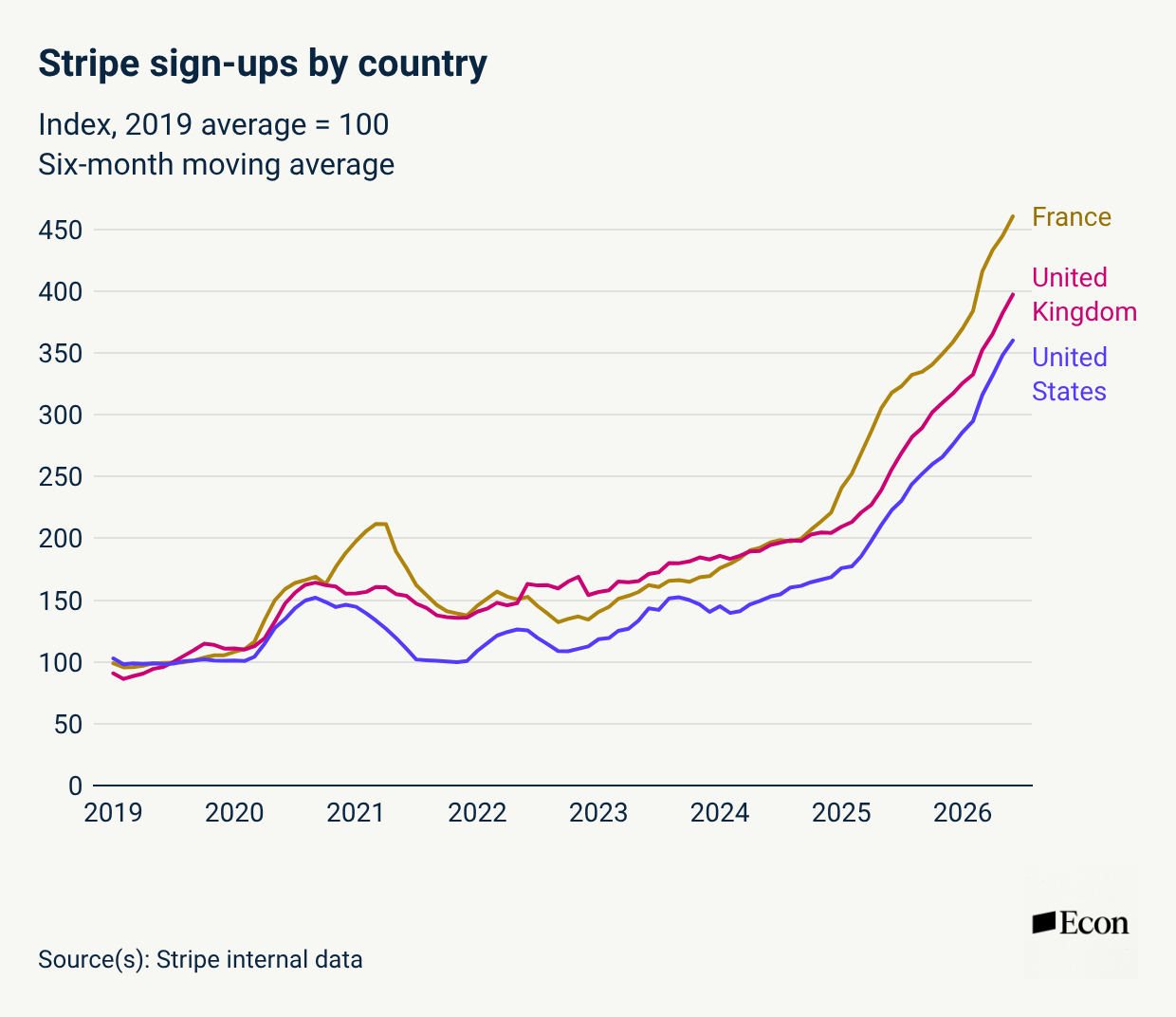

Stripe data is consistent with an acceleration in UK business creation

Stripe’s UK business sign-ups have been growing rapidly in the last few years, tracking the surge seen in the US and France almost exactly. In the last two years, UK business sign-ups have doubled.

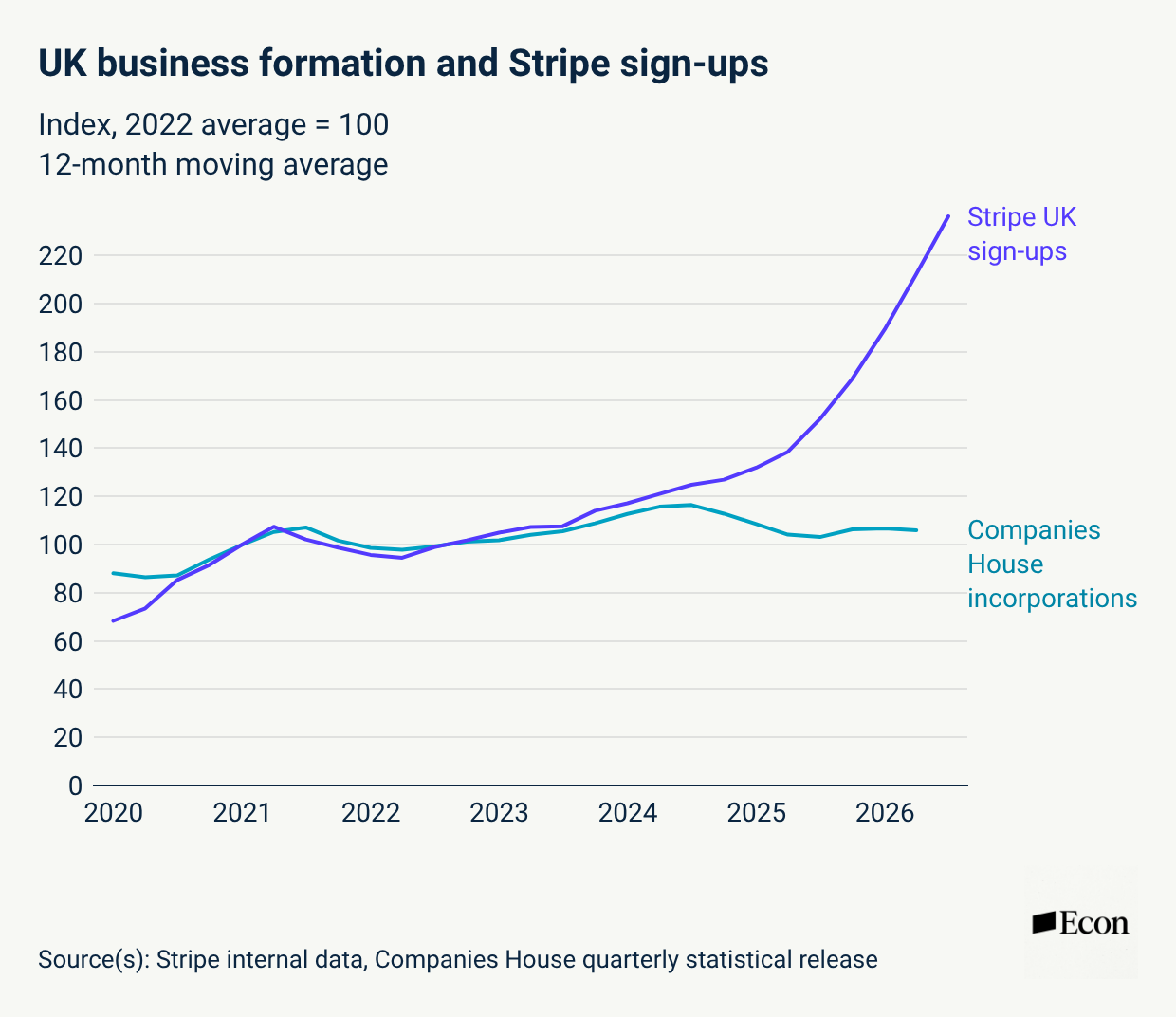

How do these trends compare to Companies House incorporations? During the early post-pandemic years Stripe signups tracked incorporations closely; since 2024 they have diverged sharply.

While this Stripe data is a strong signal of growing underlying business formation in the UK, it is possible that Stripe could simply be increasing its market share of existing UK businesses, or capturing a greater share of new UK businesses that are forming. Our analyses suggest neither of these is first order. While migrations onto Stripe in the UK are indeed growing, migrations as a share of Stripe sign-ups are declining. Put otherwise, the surge in sign-ups predominately represents net-new business activity. In addition, the surge in signups is so large that, absent an underlying surge in business formation, the probability of the implied share-gain over such a short time frame is low.

Conclusions

The UK is likely experiencing an increase in solopreneurship broadly in line with what we see in the US, France, and many other markets.

Solopreneurship in the UK is poorly captured by official statistics. If, as early analysis suggests, a surge in solo-run businesses turns out to be a major feature of the economic transition driven by AI, the UK’s inability to track it creates a major policy and economic blindspot.