The decline of travel agents

A case study in job displacement

One of the biggest uncertainties in labor markets today is whether AI will displace human work at scale. The overall evidence so far is mixed and preliminary. Labor markets—complex under normal conditions—are even more so during technological shocks.

Some occupations, like radiologists, have proven more resistant to technological displacement than expected. Others, like bank tellers, did eventually succumb—just to later and different shocks than most predicted.

Sometimes though, displacement happens in straightforward ways, as with travel agents. Airline deregulation in the late 1970s both complicated booking prices and loosened rules on travel agent commissions. Together, these changes made the profession far more lucrative and boosted employment: between 1980 and 2000, travel agent jobs tripled, peaking at about 340,000. But then a prolonged structural decline set in, driven by a one-two punch: airlines began cutting agent commissions on ticket sales in the early 1990s; and internet platforms like Expedia, Travelocity, and Priceline emerged, advertising that everyday consumers could now access the same reservation systems agents once monopolized. The loss of clients to online providers and reduced commissions led many brick-and-mortar agencies to downsize or shut down entirely.

So the decline of travel agents was driven largely by technological displacement. AI is a very different kind of shock from the internet of the 1990s, and its effects on labor markets may turn out to be quite different too. But the story of the travel agent is still instructive, because it demonstrates what happens to workers when a technology renders their profession obsolete. As it turns out, the story is not entirely bleak.

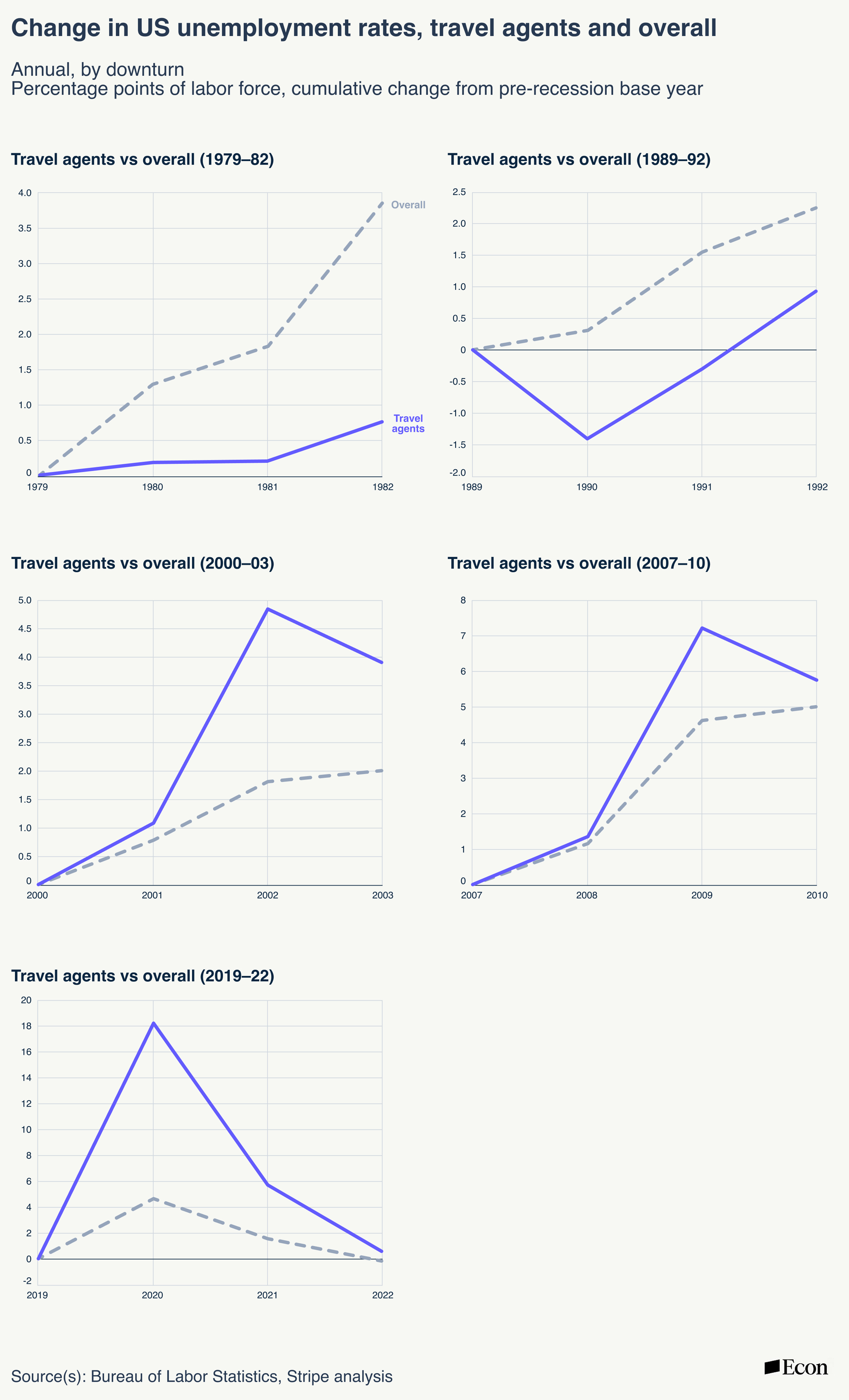

1. Travel agent layoffs came in recessionary bursts, not a gradual decline.

Widespread displacement of travel agents didn’t happen immediately during the dot-com boom. Rather, it was the bust that drove displacement. In the wake of the 2001 recession, employment in the travel agency industry1 fell precipitously and did not claw back prior losses. By the eve of the Great Recession in 2007, there were already nearly 40% fewer workers in travel agencies than at their dot-com peak. Four years later, employment was at less than half of its peak, and today travel agency jobs are 60% lower.

2. Travel agent unemployment rates are still low in good times, but are now higher in bad.

While travel agent employment has declined steadily, so has the travel agent labor force, indicating that many agents have changed careers since 2000. As a result, the unemployment rate of travel agents—measuring the utilization of their labor force—was just 2.8% in 2025, lower than typical even before the dot-com boom.

But this low rate comes with a major asterisk. Travel agent unemployment has become far more sensitive to economic downturns. Before 2000, travel agent unemployment rates typically rose by less than the overall rate during downturns. Between 1979 and 1982, for example, the travel agent unemployment rate rose only 0.8 percentage points despite the overall rate jumping nearly 4 percentage points. The pattern repeated over 1989–1992, with travel agent unemployment rising only 0.9 percentage points versus 2.2 overall. But after 2000 the pattern flipped: the travel agent jobless rate spiked 3.9 percentage points over 2000–2003 versus 2 overall, 5.8 versus 5 over 2007–2010, and 0.7 versus 0 over 2019–2022.2

3. Pay for travel agents has outpaced overall wage growth as they have shifted to higher-value bookings for wealthier clientele.

As the market migrated online in the late 1990s and early 2000s, the remaining human travel agents pivoted sharply upmarket. They adapted by charging planning and membership fees and aligning with luxury consortia like Virtuoso to offer high-end clients exclusive upgrades, complimentary amenities, and personalized services that no algorithm could replicate. This shift is reflected in wages. Average weekly earnings at travel agencies were 87% of overall average weekly earnings back in the heyday of 2000. By 2025, the ratio had reached 99%, meaning travel agency wages had outpaced the rest of the private sector over that span.

4. Economy-wide employment has fully recovered

Travel agent employment is down by more than half from its dot-com peak. This caused hardship for agents forced to switch careers and facing greater risk of joblessness. Decades later, however, the dot-com boom has not lowered aggregate employment. While the employment-population ratio has fallen five percentage points since 2000, this is entirely because of population aging. Adjusted for today’s demographics, the employment rates of 2000 look virtually identical to the present. As travel agent jobs disappeared, new jobs emerged elsewhere, many former agents switched careers, and young workers who might once have become travel agents went into other fields instead.

History doesn’t repeat itself, but it does rhyme. AI’s effects on the labor market may not be identical to past technological shocks, including those on travel agents. But the experience of travel agents highlights risks for us to consider. On the one hand, AI disruptions to the labor market may be delayed and not salient until (perhaps even amplified by) the next recession. On the other hand, the most negative effects may be limited to specific occupations rather than broad-based, and as prices and wages adjust, those occupations may even look more favorable over time. But that’s of little comfort to anyone displaced in the near-term. These risks suggest the policy focus should be more weighted towards easing transitions for whatever displacements do take place rather than assuming mass unemployment.

This chart shows industry payroll employment for NAICS sector 56151: Travel Agencies. This is distinct from travel agent occupational employment, which peaked at 339,000 in 2000 according to the Decennial Census. Just over half of travel agents actually worked in payroll jobs in travel agencies in 2000. The rest worked in other industries (e.g. the airlines themselves) or were self-employed running their own businesses.

The pandemic lockdowns disproportionately hit the travel and tourism industries in 2020 and 2021; 2022 was the first year real air travel spending exceeded 2019 levels in the US.

Seems like it lines up with the Autor/Thompson expertise framework pretty nicely. Less expert tasks (flight booking) were automated, while more expert tasks (coordinating with wealthy clients) weren't, so employment fell and wages rose.

The big question for welfare, which there's probably no good data on, is how successful the displaced agents were at switching professions.

How greatly has travel spend expanded in the US since the 90s? What is the counter factual total agent employment in that world?